The Generational Wealth Divide

A striking feature of today’s property market is the concentration of housing wealth among older generations. According to the latest assessment from Savills, owner-occupiers aged 60+ now hold a record estimated £2.89 trillion of net housing wealth across the UK.

In total, those over the age of 60 control 56% of all owner-occupier housing wealth, while those over 75 control 23%. This concentration of property assets has significant implications for market dynamics and intergenerational wealth transfer.

![Chart showing distribution of owner-occupied housing wealth by age]

The data highlights a fundamental disconnect in market participation: while baby boomers (born 1946-1964) make up 44% of homeowners, they accounted for just 18.5% of homebuyers last year. This means only one in 57 baby boomer homeowners moved house in 2024, creating a significant bottleneck in housing supply.

Over the past decade, the baby boomer generation has continued to build wealth and pay off mortgage debt. These strong equity levels have provided them with a financial buffer during the cost of living crisis, reducing the pressure to downsize. Additionally, with many older homeowners occupying properties larger than their current needs, there appears to be little market incentive for them to move.

The Bank of Mum and Dad

This concentration of housing wealth has led to an interesting market dynamic: intergenerational wealth transfer is increasingly supporting first-time buyers. The substantial equity held by older generations has enabled many to gift deposits to family members looking to get onto the property ladder, helping to explain why first-time buyer numbers remain robust despite affordability challenges.

This “Bank of Mum and Dad” phenomenon has become a critical factor in sustaining market activity, with family support often making the difference between renting and homeownership for many younger buyers.

Buying vs. Renting: The Cost Equation

The latest research from Hamptons reveals that the cost of renting versus buying a home in Great Britain has now reached an equilibrium point. With mortgage rates hovering around 5%, the average monthly mortgage payment on a 90% loan-to-value (LTV) mortgage (£1,328) is now slightly cheaper than the average rental payment (£1,356).

This represents a significant shift from just two years ago, when renting was £48 per month cheaper than buying. According to Hamptons’ analysis, since January 1987, there have only been three occasions when renting has been cheaper than buying.

This cost parity between renting and buying, combined with the continued rise in rental prices, is providing a strong financial incentive for tenants to pursue homeownership. This trend helps explain why first-time buyers continue to enter the market at robust levels despite broader affordability challenges.

House Price Trends

The latest Rightmove House Price Index showed a 1.4% monthly increase in average asking prices in April 2025, a larger than usual rise for this time of year. This has established a new record for asking prices – the first since May 2024 – despite stock levels being at their highest since 2013.

Rightmove reports that mover activity remains resilient, with new buyer demand up 5% year-on-year and the number of new sellers coming to market up by 4%. Similarly, Zoopla reports a 1% increase in buyer demand, with sales agreed being 6% higher and the stock of homes for sale 12% higher than at this time last year.

However, Zoopla also notes that buyer demand is cooling, and the continuing expansion in the supply of homes for sale is likely to slow house price growth, though they still expect continued growth in the number of sales agreed.

Market Balance Indicators

Several metrics suggest a gradual shift toward more balanced market conditions:

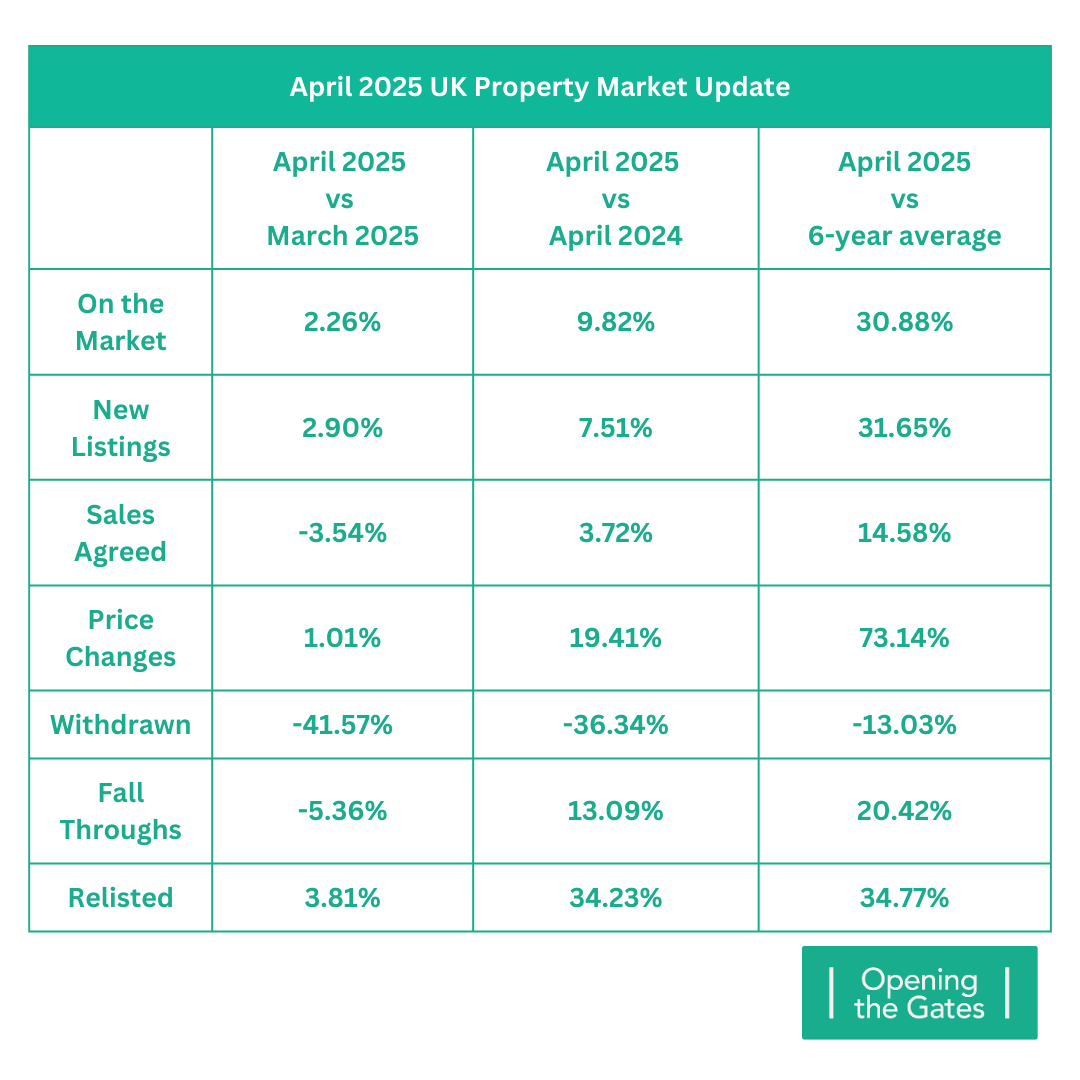

- Price Changes: There has been a 19.41% rise in the number of price reductions compared to a year ago and a 73.14% increase on the six-year average for April. This indicates growing price sensitivity among buyers as inventory levels rise.

- Stock vs. Sales Ratio: The higher number of sellers entering the market and fewer properties withdrawing has increased competition among sellers and expanded choices for buyers. This dynamic is likely to constrain excessive price growth.

- Price Expectations vs. Reality: While 46% of consumers expect prices to continue rising over the next 12 months (BSA survey), the increasing frequency of price reductions suggests a disconnect between seller ambitions and market reality.

These indicators point to a market that is gradually shifting from the strong seller’s market of recent years toward more balanced conditions.

Housing Costs and Affordability

Barclays Property Insights data shows that housing costs, including rent or mortgage payments, council tax, energy, and other bills, now make up 28% of income across the UK, rising to over a third (36%) amongst renters.

Nearly three-quarters (73%) say these expenses have risen in the last 12 months, averaging an extra £126 a month, or £1,516 a year. This ongoing pressure on household finances is contributing to some softening in consumer confidence.

However, with wage growth (5.6%) outpacing inflation (2.6%), there is gradual improvement in real disposable incomes, which should help support market activity through the remainder of 2025.

Looking Ahead: Market Outlook

As we assess the prospects for the UK housing market through the remainder of 2025, several key factors are likely to influence performance:

- Interest Rate Trajectory: With the Bank of England expected to cut rates multiple times this year, mortgage affordability should gradually improve, supporting transaction volumes.

- Supply-Demand Balance: The continuing increase in available inventory will create more choice for buyers and limit excessive price growth, but strong underlying demand should prevent any significant price corrections.

- External Economic Factors: The impact of Trump’s global tariff policies represents a significant uncertainty. While potentially dampening economic growth, lower inflation could accelerate interest rate cuts, creating offsetting effects for the housing market.

- First-Time Buyer Support: The combination of cooling rental growth, improving mortgage availability for high LTV borrowers, and continued intergenerational wealth transfer should maintain the critical first-time buyer segment of the market.

- Mortgage Affordability Testing: Zoopla’s identification of a potential relaxation in lender stress testing (from 8-9% to 6.5-7%) could significantly boost buying power by 15-20% if implemented widely across the market.

Conclusion

The UK housing market has demonstrated remarkable resilience in the face of significant headwinds, from the conclusion of stamp duty relief to global economic uncertainties. While there are clear signs of a gradual shift toward more balanced conditions, the fundamentals remain broadly supportive of continued activity.

The concentration of housing wealth among older generations will continue to shape market dynamics, both constraining supply and enabling intergenerational support for first-time buyers. Meanwhile, the equalization of rental and mortgage costs provides a compelling case for homeownership for those able to overcome the deposit hurdle.

As we look ahead, the market appears well-positioned for modest price growth and stable transaction volumes, provided sellers remain realistic with pricing expectations and economic conditions continue to support consumer confidence. The projected reductions in interest rates, combined with potential adjustments to affordability assessments, offer significant upside potential for market activity through the remainder of 2025.

However, the resilience of the property market will be tested further by the impacts of global trade policies on the UK economy in the coming months. Monitoring these external factors alongside domestic housing metrics will be essential for navigating the evolving landscape of the UK property market.